Market Update – 12th November 2025

Q3 2025 Market Update

The third quarter of 2025 has brought a cautious sense of optimism, though many warning lights do still remain. Globally, while inflation is gradually easing, there have been stubborn factors at play making it stickier than central banks would like. For instance, wages, energy and services costs continue to keep policymakers on their toes.

In terms of growth, globally it has remained positive this quarter, albeit uneven. Continued political uncertainty, trade tensions and high energy costs are weighing on business confidence, but labour markets seem to be holding up in most major economies. That being said, there are signs that softening is starting – for example, in the U.S. and the UK.

Against this backdrop, the World Bank and IMF revised their estimate for global economy growth to 3.1% in 2026, up from 3%. The increase comes from expected stronger spending in some countries, such as Germany, where governments are increasing their fiscal support. Meanwhile, global trade activity has picked up ahead of expected tariff changes later in the year, providing a short-term boost to manufacturing and exports.

Still, while overall growth is positive and continues to surprise to the upside, recovery remains bobbly. For instance, over in the U.S., the world’s largest economy contracted in the first quarter of 2025, had a strong bounce back in Q2 and then grew by a steadier pace in Q3. In Europe, growth has been more moderate, where weaker business confidence (despite healthy labour markets) has led to subdued investment, holding the region back.

Emerging markets have had a varied picture too. India and some Southeast Asian countries have enjoyed growth, thanks to strong domestic demand coupled with foreign investment. China, meanwhile, has lost some of the momentum seen previously with slower growth in exports, property investment and consumer spending.

Inflation and interest rates

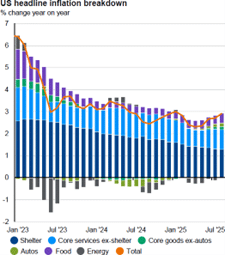

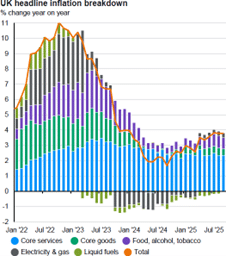

Overall, global inflation numbers continue to fall, but not as fast as central banks would like. Inflation is not yet where policymakers would want it to be, as food, services and wages remain higher. There is variation across countries when it comes to goods price inflation, which in some areas has come down sharply.

When looking at different countries specifically, in the U.S., inflation remains above the Federal Reserve’s 2% target. The country’s price rises are a good example of where wage growth and rising rents continue to keep inflationary pressures high. For the UK, inflation is uncomfortably high too, where it currently sits at around 3.8%. The persistently high figure is primarily down to energy bills, food prices and household costs – all of which are proving slow to come down.

Across the Eurozone, inflation figures are starting to moderate more convincingly. However, even there, the ‘core’ measure (which excludes food and energy) continues to decline at a slower pace. So, while things are starting to improve for consumers, it’s not yet an easy ride. However, confidence is rebuilding from previous lows, but households are still cautious about spending given increases in borrowing costs and lingering economic uncertainty.

Central bank dynamics

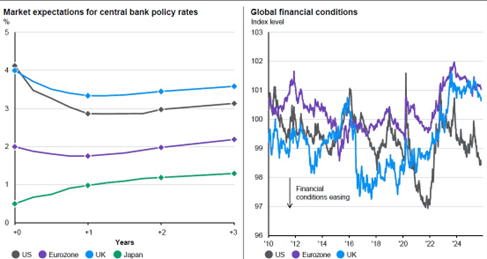

Persistent inflation makes life for central banks more complicated than they’d like. Moreover, markets would love to know when and how fast policymakers will start cutting interest rates, but that’s tough to predict until there are clearer signs that inflation is under control.

This quarter, after holding rates for the majority of the year, the Federal Reserve made a cut of 0.25%, so that its key rate now sits in a range of 4.0-4.25%. With the labour market starting to soften, there was reason to begin easing, however officials stressed that inflation is not yet fully under control – potentially meaning a slower pace of rate cuts in the future.

Here in the UK, the Bank of England held rates at 4%. The BOE cited persistent inflation as a reason for the hold as well as uncertainty to inflation’s path. In addition to holding rates, it also announced it would slow its quantitative tightening (where it sells fewer government bonds known as gilts) to help calm gilt markets after a period of volatility.

Equity markets in Q3 2025

Global stock markets continued to climb this quarter, building on their earlier rebound in Q2. After a shaky first half to the year, following Trump’s Liberation Day tariffs sparking trade fears, equity markets seemed to find solid ground again.

In terms of best performers, China and Japan produced notable performances, helped by cheaper valuations and a weaker U.S. dollar. Smaller companies and ‘growth’ stocks did well, outperforming larger companies. In the UK, equities continued their strong 2025 performance supported by a wave of company share buybacks and renewed interest from overseas investors, particularly from the US.

Technology and artificial intelligence (AI) continued to play a starring role this quarter. Investors perceive these firms to have the ability to produce strong earnings growth, with many of those stocks performing well this quarter. Other sectors which caught the attention of investors in the third quarter, and generally led the global equity markets, include consumer discretionary, real estate, energy and financials.

A few major themes shaped performance during Q3:

- Rate cut anticipation: Markets typically respond well when a central bank seems ready to shift from tightening or holding to easing interest rates.

- The weaker US dollar: The US dollar, which had weakened against other currencies earlier in the year, appeared to stabilise in the third quarter thereby helping US equity returns when translated into sterling.

In short, the equity market recovery that began earlier in the year gathered pace, supported by optimism that the next phase of monetary policy will be gentler.

Fixed income markets in Q3 2025

Bond markets have been calmer this quarter than earlier in the year, though they are still sensitive to economic data and central bank signals.

In the US, yields on longer-dated Treasury bonds ended the quarter roughly where they started, having swung during the summer as investors reacted to inflation figures and jobs reports.

Across the Eurozone, yields on government bonds (or “bunds”) were stable, with inflation now close to target. In the UK, gilt yields fluctuated more sharply as the Bank of England maintained its cautious stance, but later eased when the Bank slowed the pace of bond sales.

Corporate bonds (those issued by companies rather than governments), remained broadly stable, with continued investor demand for income. High-yield bonds (those offering higher returns in exchange for more risk) produced mixed results depending on the sector and region.

In emerging markets, bonds performed well where governments pursued pro-growth policies and currencies remained stable. In contrast, countries facing fiscal stress or weaker currencies saw outflows.

Looking ahead

As we move into the final quarter of 2025, the broad picture is one of transition. Inflation is falling, but unevenly. Growth is steady, but slower than before. Central banks are edging toward rate cuts, but carefully.

For investors, like us, this environment offers both challenges and opportunities:

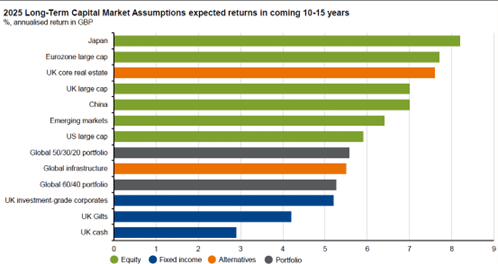

- Equities are likely to deliver solid long-term returns, but we expect more dispersion between sectors and regions, meaning diversification is key.

- Bonds have returned as a meaningful source of income, after years of ultra low

We continue to see diversified portfolios as the best way to traverse through volatile markets, so we can capture opportunities but avoid overexposure to any one theme or market. Diversification helps us to weather risks where they remain – such as continued geopolitical tensions, unpredictable inflation or high energy prices.

We do have a cautiously optimistic stance, however. We anticipate productivity gains driving growth and a normalisation of monetary policy creating a supportive backdrop for investors with a long-term view. After years of extremes such as ultra-low interest rates, the pandemic and inflation spikes, the global economy is settling into a new routine. One with a slower, steadier, more balanced rhythm.

As such, our focus is on keeping portfolios positioned for this new backdrop. We will continue to diversify across regions and asset classes so that we can build portfolios that are resilient against near-term and long-term risks. Doing so means we can take advantage of any opportunities that appear as the next stage of the cycle unfolds.

This document is marketing material issued and approved by Square Mile Investment Services Limited (“SMIS”) which is registered in England and Wales (08743370) and is authorised and regulated by the Financial Conduct Authority. The independent research is provided by Square Mile Investment Consulting and Research Limited (“SMICR”) which is not authorised or regulated by the Financial Conduct Authority and does not undertake regulated activities. Titan Square Mile is a trading style of SMIS and SMICR. SMIS and SMICR are wholly owned subsidiaries of Titan Wealth Holdings Limited (Registered Address: 101 Wigmore Street, London, W1U 1QU).

Our thoughts expressed in this document relate only to the portfolios we manage or advise on, on behalf of our clients, and as such may not be relevant to portfolios managed by other parties.

This document is issued to professional advisers and regulated firms only and it is the responsibility of the professional adviser or regulated firm to determine if it is appropriate for this document (or any part of this document) to be provided to their underlying client base. It is published by, and remains the copyright of, SMIS. SMIS makes no warranties or representations regarding the accuracy or completeness of the information contained herein. This information represents the views and forecasts of SMIS at the date of issue but may be subject to change without reference or notification to you. This document does not constitute investment advice, a recommendation regarding investments or financial advice in any way and shall not constitute a regulated activity for the purposes of the Financial Services and Markets Act 2000. Should you undertake any investment activity based on information contained herein, you do so entirely at your own risk and SMIS shall have no liability whatsoever for any loss, damage, costs or expenses incurred or suffered by you as a result. SMIS does not accept any responsibility for errors, inaccuracies, omissions, or any inconsistencies herein. Past performance is not an indication of future performance.

Source of data: Titan Square Mile, unless otherwise stated. Date of data: 30th September 2025.